On being wrong

Why are US stock indices at all-time-highs? Its hard to believe that its because the wanton destruction of global energy infrastructure is close to ending.

First, as a reminder, I had argued that there was little or no overlap between US/Israeli and IRGC negotiating positions, which led me to conclude it would be difficult to reach an agreement. One might have argued that the US/Israel objective was to meaningfully weaken the IRGC/Iran, while the key IRGC objective was to reestablish deterrence. If the IRGC fails to do this, then they would ultimately be doomed, because the US/Israel would be able to use its strategic dominance to indulge in periodic “mowing the lawn”, preventing normal economic development for a further extended period of time. In this scenario, the prospects for senior (or even mid-ranking) figures within the IRGC would be bleak.

Iranian tactics are actually very simple. Maintain a choke hold on global oil flows while threatening tat-4-tat strikes on Gulf oil infrastructure if Iranian infrastructure is targeted. So, while they cannot defend their own infrastructure from strikes, they appear able to impose symmetric (if not higher) costs on US allies in the Gulf, with collateral effects in the rest of the world. An example of this was when Israel hit some of Iran’s South Pars gas field infrastructure, the Iranians retaliated by striking Qatar’s Ras Laffan Industrial facility impacting Qatari LNG production (and two KSA refineries). It was reported that Qatar lost 17% of its LNG export capacity. Perhaps an even better example of their tit-4-tat tactic was the retaliatory strike on part of the Jubail Industrial City which is (was?) responsible for 7% of KSA GDP. That strike followed strikes on Iran’s Assaluyeh petrochemical plants. The Jubail strike took place overnight on April 6th/7th. The US-Iran ceasefire (two-week truce) was announced on April 7th and came into effect on the April 8th.

By restricting flows of energy out of the Gulf, Iran has created an enormous disruption in global energy flows. However, that disruption involves something like a 6 to 10-week lag. As such it is only beginning to manifest. Some of the last ships to have left the Gulf, are only just reaching their destinations now. The point is the global energy trade should be thought of as a flow, and there has been a significant interruption in that flow. I am told that refineries usually keep between a month and two months feedstock in inventory. I’m also told (H/T Ann T) that there was significant slack within the US, and that that slack is now being utilized to mitigate the disruption to global supplies. That mitigation might amount to maybe 2mn bpd of oil and oil products, and that has stretched timelines for when product shortages become acute. That said, other industries may not have had the same amount of unused capacity: such as with methanol, helium, urea, or sulfuric acid. We will inevitably experience significant supply chain disruption: that’s baked in the cake. The question is how long and deep that disruption will be. If we achieve some kind of negotiated peace deal soon, then the extent of the value-destruction will be minimized. If we don’t, then we might see another round of tit-4-tat infrastructure destruction, with all that implies for global supply chains.

But while I still believe all this is true, this piece has a different focus. In the absence of any meaningful overlap between US and IRGC positions, I had assumed that this war would drag on till harms were significant enough to force one side to capitulate. But then I made the mistake of assuming that this kind of catastrophic supply chain/energy shock would be negative for earnings (probably) and therefore negative for stocks (nope!). I do think there will eventually be a deal, and it might look a bit like this as Barak Ravid’s tweets seem to point the way to the eventual structure of that deal. I assume we will get to a deal because it’s the most rational course. That said, there are still some serious potential risks to this assessment. Both sides have “tooled up” again in an effort to encourage the other to show flexibility in negotiations.

One of the big advantages of trading is that there is a very simply way of determining who is wrong and who is right. In this, trading is very different to say, theology, politics or “investing”. You might consider this paradoxical, because “investing” almost definitionally implies some kind of rational process. But it is precisely because rational “processes” take time to prove out that it becomes tricky to keep score. You must factor in the inevitability of “drawdowns” with any rational “process” and so you need time to evaluate the process (or investor). This leads us to the concept of “conviction”. Conviction can be defined as a firmly held belief or opinion, and if you wanted to quantify it as applied to investing, you might do so with reference to the scale of the short-term losses you were willing to accept because you remain perfectly convinced that the market is wrong. If your process always works, then it will usually be a mistake to unwind a trade for a loss. Ultimately the market will come round to your point of view. After all, you are “right”.

When I was young, I was “blessed” with plenty of “conviction”. There were plenty of times, when I disagreed with others but was not in the slightest bit worried because I had “conviction”. I “knew” I was right. Of course, I knew no such thing. I was just too stupid to understand that what I thought was superior understanding was usually just inferior logic. But as I got a bit older, I started asking myself inconvenient questions about “conviction”. Do others have “convictions” too? If so, how might I recognize when I was right, and they were wrong? Another formative experience was a game of 3-card brag in a North London minicab office (what’s a “minicab office” grandad?). I won the then unthinkable sum of GBP5, but I couldn’t shake the dreadful realization that I could just as easily have lost - it’s the good hands that are the most dangerous. If he really did say it, Mark Twain’s “It Ain’t What You Don’t Know That Gets You Into Trouble. It’s What You Know for Sure That Just Ain’t So” is an excellent expression of this. And then there is the St. Petersburg Paradox which serves to remind us that the market can remain irrational for far longer than we can remain solvent (or under-briefed).

So, for several reasons, I am now deficient in “conviction”. In some ways it’s a handicap, because it makes it far more difficult to make very big, life-changing bets. However, it does have certain advantages, not the least of which is that my wife can (usually) sleep at night. I tend not to “bet the farm” on any one hand, no matter how good it is. I think I am generally more right (righter?) than not, but I have yet to come across any trade where I want to bet the house, let alone the farm.

I was bullish energy and bearish equities because of events in the Straits. I pared down my risk positions (early) and took on long energy bets. None of those trades is onside right now. I doubted the Iranians could consider opening the Straits without at least trying to give the US a bloody nose. In fact, Araghchi clearly felt there was some advantage in opening the Straits a few days ago. That advantage might have been to present Iran as rational actors who are open to a deal, heading off some rather more costly alternatives for all sides. Regardless, my wife is deeply unimpressed. She now wants Corvin to manage her money.

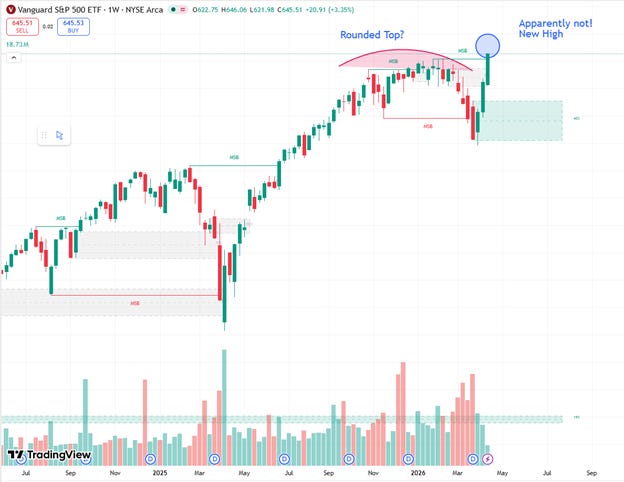

But the question I want to focus on is how did I get something so important, so terribly wrong? I ask this question not just because I am a miserable, self-hating pessimist (although if the cap fits) but because diagnosis is often the first step to cure. I think there is a huge amount of value in trying to understand why the US equity market might be trading new highs.

Is it fiscal policy?

My first observation is that trading new ATHs makes no sense if the only thing that has changed was the war between Iran and the US/Israel. Removing a sizable negative (war and the closure of the Straits) shouldn’t drive equities higher, all else equal. The net effect of the war was to destroy a meaningful amount of global productive energy infrastructure and reduce global output. Of course, we did also increase the supply of USTs and Israeli government bonds, and I would imagine the same is true of Iranian public debt, although it’s not a figure I have to hand. I don’t think it controversial to say that while relief rally makes sense, new all-time highs don’t, other than because (as Corvin reminds me) stocks generally go up.

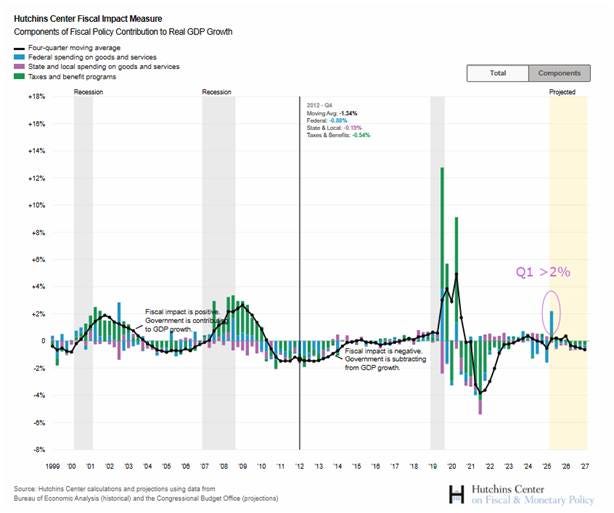

My first guess was that it was fiscal, which we know from Covid can be astonishingly effective in driving asset bull markets. The Hutchins Fiscal Impulse measure tells us that Q1 added 2.06% of GDP annualized, which is the largest positive fiscal impulse since Q1 2021.

This fiscal impetus is now behind us, but its effects on financial markets are probably still feeding through. Over the last few weeks TGA flows have added to liquidity, but it’s tax week and there is now a lot of money piling up in the TGA. Even more potential ammo for risk markets.

There is another fiscal line item that might be worth breaking out. US debt service payments are now approaching the single largest component in the US deficit. Treasury interest rate payments will have a very high propensity to find their way into securities markets, simply because they will be disproportionately held by those with very low propensities to consume. Given Federal Debt to GDP is now over 120%, higher rates result in a meaningful flow of dollars from the government sector to the private sector. The Treasury’s monthly budget data showed $519bn in interest payments in the 6 months to March 2026, 6.1% higher than the prior year. Debt service is now reportedly a bigger component than military spending although we should probably check again in a few weeks, given the cost of Tomahawks and Patriot interceptors.

This fiscal explanation doesn’t sit well with me: it’s unsatisfying because the rally doesn’t quite match up to the fiscal impulse. If you superimposed charts of the two, they wouldn’t align well. Earnings have been ok, albeit that the upward revisions which have accommodated the rally do appear highly concentrated (the Energy and Technology sectors). Consumers do not appear to be ok: metrics of consumer discretionary spending continue to be poor. Unsurprising given wages are barely keeping pace with measured inflation. Food and energy inflation is hard to substitute away from, so the impact of higher inflation is hitting the less affluent harder than the averages suggest. Perhaps the most indicative diagnostic is that bonds have been soft. The rates market has been busy pricing-out Fed rate cuts and pricing in some half-hearted hikes. Personally, I will believe in a hawkish Fed when I see one, but this is simply an acknowledgement that inflation will be higher this year. I agree that the CPI inflation we see is likely to be transient, but I can’t help but notice the regular opportunities to speak about “transient” inflation since 2019. 3% really does seem to be the new 2%, and it’s not immediately obvious why 4% won’t end up being the new 3%. It will end up being up to Warsh. But the broader point is still valid. Overall, fiscal policy has accommodated higher earnings (via higher investment and energy costs) even if it was not sufficient to boost consumer sentiment.

I think you know that I think lower global trade necessarily implies lower global capital flows, and that in those circumstances, the US (among others) will have to adjust to an environment of scarce global savings, and deteriorating terms of trade. If this is correct, it would not be surprising that the market value of some past accumulated claims on global savings might be haircut. US debt service is now a meaningful flow into US assets markets. And US spending is likely to continue to surprise to the high side given spiralling military spending. Perhaps the best way to make sense of what we are seeing is to frame it as another leg of the “debasement trade”: hence the rotation out of bonds into equities. By debasement trade, I mean a shift in investor preferences towards inflation-resistant assets over inflation-vulnerable assets. If this hypothesis is right, commodity prices will continue to climb, as would stocks with pricing power. Bonds, not so much. One way or another we are going to have to generate far more domestic savings than we have in the recent past. Put another way, the US (and the rest of the G10) will not be able to rely on the kindness of current account surplus strangers to fund their deficits at reasonable rates. Savings rates will rise in the US or deficits will have to fall (unlikely!). The question is how much real rates need to rise to persuade Americans to save?

There is a school of thought that a “strategic defeat” for the US in Iran would mean a weaker dollar. Don’t ask me what the definition of strategic defeat is, although I did notice the visit of the Taiwanese KMT leader to Beijing. What I do think is that recent events have added a lot of supply to US Treasury markets and not done much to increase demand. Foreigners want US equities, not the bonds. Gulf Kingdoms (and Iran) will want to rebuild their damaged infrastructure rather than buy more USTs. In the absence of a US recession, real yields do seem to be stuck above 2.5%. That’s going to make Warsh’s job a lot harder. In the meantime, sit back, keep your position sizes manageable and enjoy the top-quality trolling!

It is a mistake to assume the stock market is rational. Otherwise the traders wouldn't talk about the "animal spirits." Better to talk about insider information and riding on the coattails of the insiders.

The trolling is really quite something. This one came into my feed a few days ago:

https://youtu.be/hM8k8NaJTjQ?si=oa0sniERtk2vUldE

I wonder if Pump watches these... 🙃